Current Market Analysis of the Overall U.S. Housing Market (2-21-2025)

Report on Buying and Renting (Scroll Down for Report)

Presently, home prices are traded at a significant premium. Rents, however, are near where statistical models predict. Thus, it is reasonable to assume most new households and those moving to new locations around the country will likely rent initially as opposed to owning. Analysis is below. Author comments and observations are at the end of the report.

The University of Mississippi

Christie Kirkland Walker Chair of Real Estate

2-21-2025

Home Prices

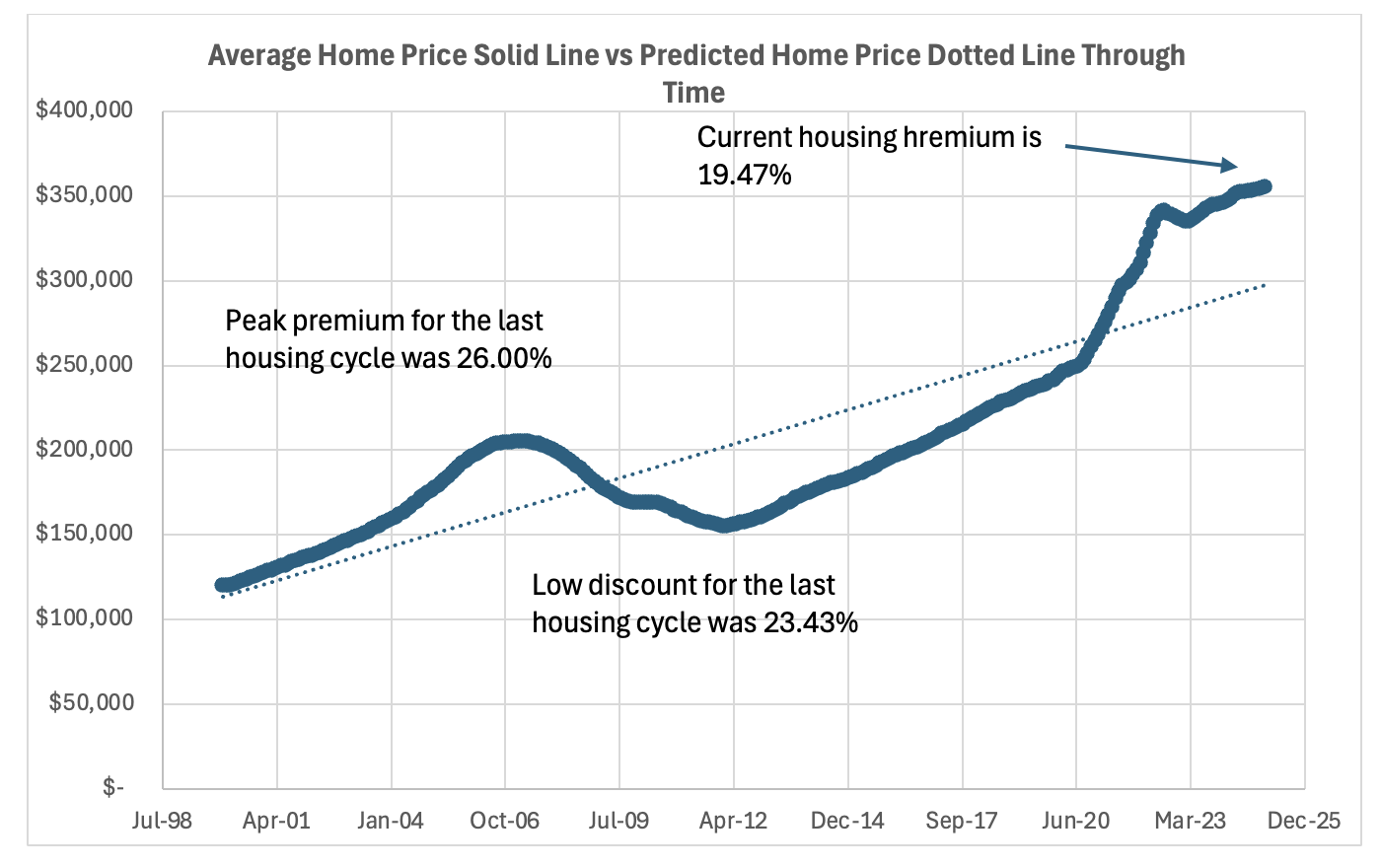

The current average closing price of residential property in the U.S. is 19.47% above the statistically modeled price for property. Housing data from Zillow is used to model a long-term pricing trend and then compared to reported average prices across time from January 2000 through January 2025.

The exhibit below depicts this analysis and other findings. The solid line provides actual average home prices, while the dotted line provides the long-term pricing trend for the U.S. housing market, i.e., predicted monthly prices. When the average price of a property is above the long-term pricing trend (predicted prices), the market is said to be trading at a premium.

When the average price of a property is below the long-term pricing trend, the market is said to be trading at a discount. The difference between the average price and predicted price is calculated as a percentage difference to allow for ease of comparison across time.

Currently, the average property transaction is closing at a 19.47% premium. At the peak of the last housing cycle, the average premium was 26.0%, and the average discount at the bottom of the last cycle was 23.43%.

The raw data source is from ZHVI (Zillow Housing Value Index) for the reporting period January 2000 through January 2025. The long-term pricing trend is developed through regression analysis taking advantage of housing’s natural mean reverting trend.

Rental Prices

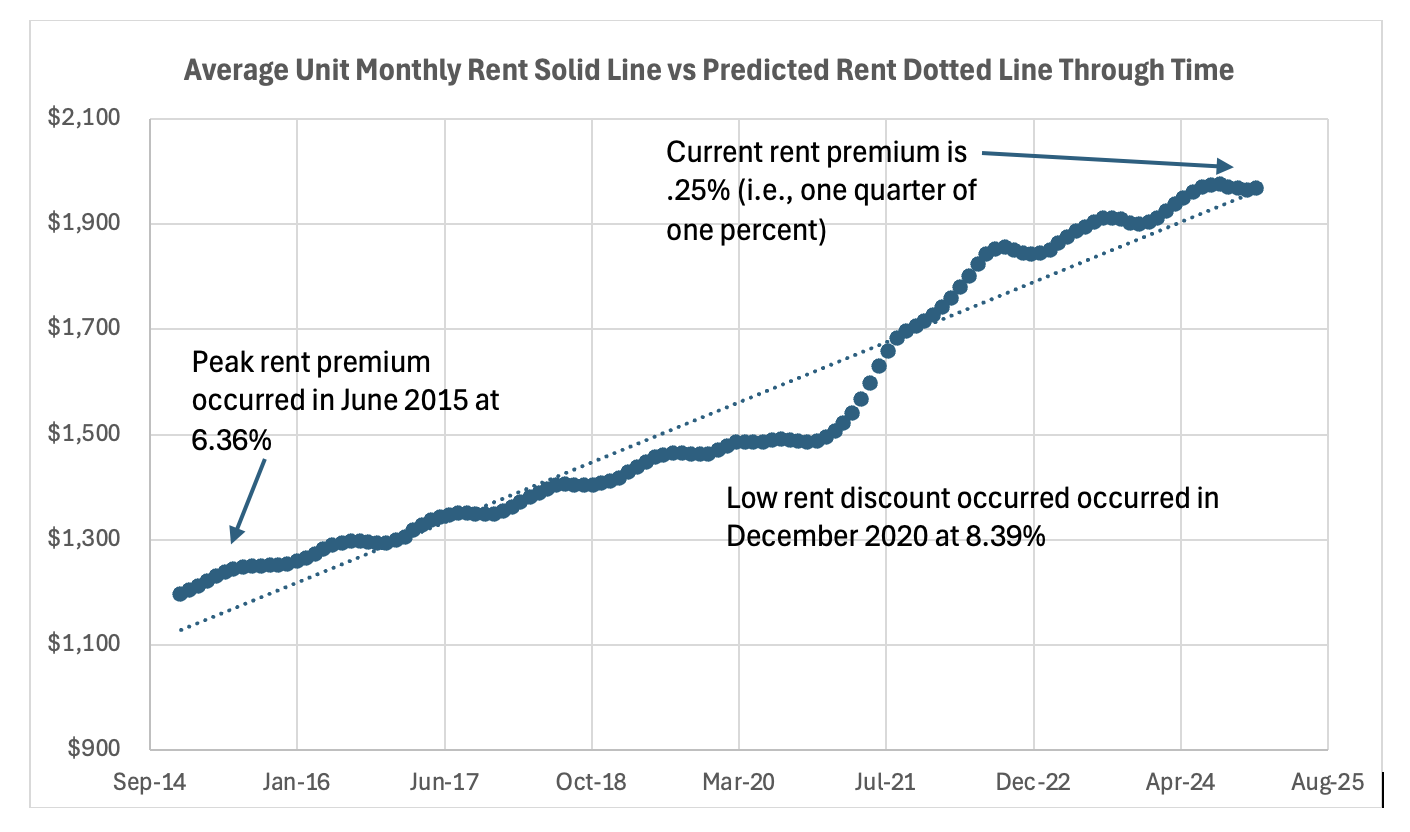

Presently, the rent for the average rental unit in the U.S. is .25% above the long-term rental trend. Said another way, to renting the average rental unit in the U.S. costs one quarter of one percent more than modeled rents. Essentially, rents are fairly priced as predicted rents and actual average rents are nearly equal.

Rent premiums and discounts are calculated statistically in the same manner as housing price premiums and discounts. The raw data source is from ZORI (Zillow Observed Rental Index). The reporting period, due to data scarcity, is January 2015 through January 2025.

Author Observations and Comments

Saying, “rents are fairly priced” does not mean they are affordable to the typical U.S. household. While rents are reverting to their long-term pricing trend as expected, affordability is still out of reach for most households as incomes continue to lag behind the pace of growth in national rents.

The pace of development for rental units around the U.S. appears to have finally reached a point where the supply and demand for rental property is in equilibrium. This is very good news; however, the cost of owning a home remains out of reach for many households. Thus, it is reasonable to expect most new households and families migrating to other parts of the U.S. will rent as opposed to owning.

Development of new construction seems to be the main holdback to the supply of available new properties to own. High mortgage rates, economic uncertainty, housing premiums, and insufficient household incomes, among other issues, appear to have created a static environment where home prices will probably stall for the foreseeable future.

Given rents are essentially in equilibrium, ownership premiums around the country seem likely to drive more households towards renting for the near future. If this is the case, these renters should consistently save at levels equal to the amounts of money they would have otherwise put into homeownership. That is, they should invest the saved downpayment and closing costs now and regularly invest forgone ownership costs -- property taxes, property insurance, HOA fees, property maintenance cost, etc. This is so because research has shown that renting and reinvesting monies otherwise put into homeownership produces greater wealth creation, on average, than owning and building equity.

By

Ken H. Johnson, Ph.D.

Campus

Office, Department or Center

Published

February 21, 2025